Evolving Web3 Regulation for India's Future 🔮

While India's web3 industry has potential for exponential growth, to unlock this potential, regulatory support is a must. We examine the evolution of India's web3 regulations to predict its future.

Introduction

India is not only an emerging economic power but an emerging force in the web3 landscape. Why so?

India has a huge population with favorable demographics, strong internet and tech adoption, a rapidly growing economy, and a government focused on backing the tech and investment ecosystem.

India’s tech investment market saw a huge boom in 2021 and 2022 (with USD 39 billion and 26 billion cumulative funding respectively, and cumulatively 100 unicorns minted by mid-2022), with a healthy mix of consumer products for India and enterprise solutions for the world.

The number of web3 projects in India and investment in the web3 space is growing rapidly – see this industry report that Hashed Emergent co-authored with NASSCOM.

India has skilled domestic talent for building web3, with the second largest and fastest growing GitHub contributor community in the world, and the fastest growing share of web3 developers in the world.

While these unique facts make India a fertile ground for web3 development to scale exponentially, the perception of India’s regulatory environment for web3 / crypto assets has been less than ideal.

To bridge this gap between perception and potential, we:

list India’s regulatory concerns with web3,

trace the evolution of crypto asset regulation in India,

forecast regulatory trends to counter the negative perceptions, and

make a case for India to regulate crypto assets in a “technologically informed” manner.

Regulatory Concerns

While the Indian government generally supports the use of blockchains, they have concerns with the “token” or “asset” layer of this technology stack:

India’s key financial regulator, the Reserve Bank of India (RBI), does not want cryptocurrencies to replace the Indian Rupee in India’s economy and create a “parallel currency”. The RBI also wants to regulate anything that creates systemic risk in the financial system.

India has capital controls, so crypto asset trades – which are effectively unregulated and result in cross-border capital flows – are viewed with suspicion.

Web3 businesses may have inadequate controls on money-laundering and terrorist financing due to the decentralised and permissionless nature of crypto assets.

Investor and consumer protection remain a concern: web3 technology brings a new dimension of regulatory problems and opportunities, since it enables peer-to-peer transactions that are intermediary-less and borderless (and this reduces the reach of traditional regulatory bodies).

Regulatory Evolution

While India has covered some ground in its regulatory approach, it has not yet enacted any law to specifically regulate crypto assets. Existing Indian laws which implicate crypto assets (such as the Information Technology Act, 2000 and the Foreign Exchange Management Act, 1999), are ambiguous and do not address crypto assets directly.

Let’s trace the history of the Indian government’s sentiment on, and approach to, crypto assets:

2013-2017

The RBI issued warnings about the risks crypto assets posted to the economy and consumers.

2016

Despite the RBI’s warnings, the Indian government’s demonetization of the Indian Rupee in 2016 contributed to the popularity and mainstream adoption of crypto assets in India.

2017

The Indian government (which typically acts independently from the RBI) began to take an interest in crypto asset regulation and formed a body of high-level representatives from various ministries to study the crypto asset market and identify key issues and concerns, marking the first significant step in its efforts to understand crypto assets.

2018

A draft Crypto Token and Crypto Asset (Banning, Control and Regulation) Bill, 2018 was published.

Things took a steep turn for the worse when the RBI banned banks and payment service providers from providing services to crypto asset businesses. This limited the ability of Indian citizens and businesses to access crypto assets, and temporarily stunted the growth of India’s web3 industry.

2019

The Finance Minister expressed negative views on cryptocurrencies in his 2018-2019 budget speech, and the government published another draft law – which now proposed an outright ban on crypto assets.

2020

The Indian Supreme Court’s ruling in IAMAI vs RBI overturned the RBI’s ban, and this was a big win for the web3 industry.

The ruling was significant since it established these important principles:

Regulators cannot enact blunt-force bans against web3 business models.

Instead, they must tailor regulations proportionally to achieve their regulatory aims, using the least invasive measures, so that web3 projects’ business models are not effectively destroyed.

Any future attempt to ‘choke’ the web3 industry’s access to vital services like banking might get struck down by Indian courts.

If there is no demonstrable harm from which a regulator is supposed to safeguard people / entities from accessing crypto assets, then it will be hard for that regulator to move against crypto assets aggressively.

The ruling catalyzed the next wave of growth of the Indian web3 industry by boosting investor and consumer confidence – coincidentally in tandem with the beginning of a global crypto asset market bull run.

Subsequently, there were further shifts in regulatory and policy messaging:

2020

NITI Aayog, India’s foremost technology focused public policy think-tank, published a draft strategy paper which proposed adopting blockchain technology, and recognised crypto assets as unique assets with properties representing network ownership and value which are essential to public blockchains.

2021

MeitY (India’s information technology ministry) published a draft ‘National Strategy on Blockchain’. The paper delved deeper into the technology stack and identified some regulatory gaps that hindered the adoption of crypto assets, including the ambiguous nature of tokens and lack of KYC norms.

The Ministry of Corporate Affairs clarified that companies must account for and report crypto asset transactions in their financial statements.

Responding to reports that banks were still denying services to companies dealing in crypto assets, the RBI issued a circular clarifying that banks and payments services were not banned from servicing the crypto space.

A draft law to regulate crypto assets was announced – but the draft law itself was not published.

Significantly, the law’s title no longer used the word “banning”, which was the case with the previous draft law.

However, it still proposed to ban all “private cryptocurrencies”, the meaning of which is still unclear.

Confusingly, it also proposed “certain exceptions to promote the underlying technology of cryptocurrency (blockchain) and its use”.

The only thing which was clear was that the government wanted to “create a facilitative framework” for its central bank digital currency (CBDC).

2022

India introduced a tax on profits from “virtual digital assets” (a newly introduced taxonomy for crypto assets) transactions at a rate of 30%. It also required that an advance tax of 1% of the profits be deducted and paid by the seller, with the aim of creating a paper trail of buyers and sellers for AML/CFT visibility.

The key question in the market after this was: have crypto assets been de facto legalised by this tax? By this point, the answer seemed to be yes.

The RBI proposed a regulatory sandbox that was open to experimenting with blockchain technology, but explicitly excluded “cryptocurrency and crypto asset related services, trading, investing, settling in crypto-assets, and initial coin offerings”.

2023

The Indian AML/KYC law was revised to specifically recognise crypto asset service providers, and to impose KYC and AML obligations on them (which was in line with the FATF’s model laws on this subject).

The Indian government’s position now:

They seem to have understood the ‘unstoppable’ nature of the technology and the fact that key market participants are outside India and therefore, outside their jurisdiction.

Therefore, they believe that trying to regulate crypto assets in India will be ineffective unless there is international cooperation and coordination.

Crystal Ball Gazing

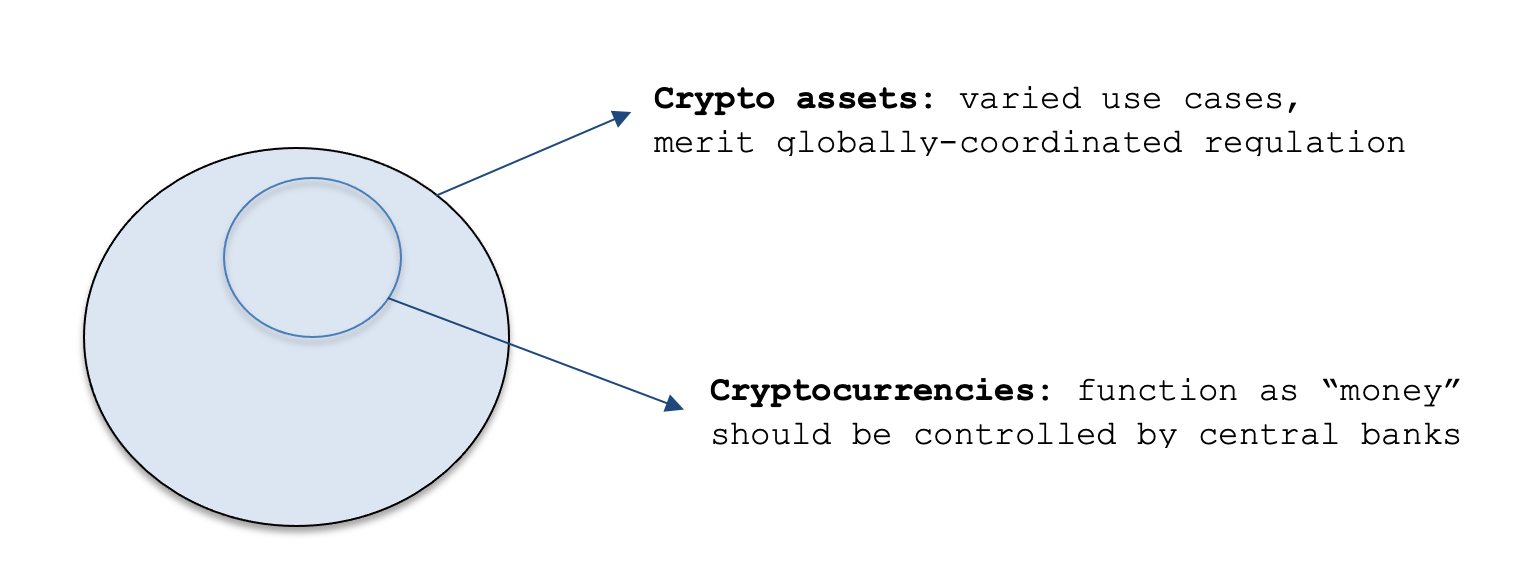

We believe that the Indian government has distinguished between the set “crypto assets” and its subset, “cryptocurrencies”, based on their use cases - and below diagram explains their view:

There seems to be a transition from the government’s initial knee-jerk reaction to a more nuanced understanding of the risks and opportunities presented by blockchain-enabled business models, crypto assets and cryptocurrencies.

Let’s gaze into the regulatory crystal ball:

We’re cautiously optimistic that the Indian government is eager to foster the growth of the web3 and blockchain sector.

After the IAMAI vs RBI ruling, the government has realised that it cannot (both practically and legally speaking) ban Indians from accessing the web3 ecosystem (for example, by banning the conversion of fiat into crypto assets).

The government has also realised that because crypto assets are easily accessible and borderless, “local” regulations will not suffice - so instead, the government will try to use its G20 presidency to drive a consensus on global regulations.

We believe that for now, the Indian government will only attempt targeted regulation to restrict the use of crypto assets in a way that directly undermines their regulatory concerns or causes systemic risks (for example, in the manner that KYC/AML compliances were recently imposed on intermediaries).

While the RBI did make some moves toward understanding crypto asset regulation with its sandbox, by and large, we feel the RBI will continue to be unfriendly to the web3 sector. Despite the RBI’s ban being overturned in court, news reports suggest the RBI is putting pressure on banks and payments players (behind closed doors) to stop doing business with companies in the crypto sector.

The RBI recently blocked Indians’ access to unlicensed lending apps by using the information technology ministry’s broad internet-regulation powers. This reminds web3 businesses which are inside the RBI’s regulatory ambit (i.e., financial services) that it may be difficult to reach a wide audience if the RBI attacks them with similar actions.

Tying all of this together, we believe since the government wants to curb “parallel currencies”, stablecoins will likely face heavy regulations consistent with the EU’s recently passed MiCA or proposed US laws. DeFi will be the next “most regulated” sector, followed by web3 gaming (the Indian regulatory approach to gaming has traditionally been tough).

We are currently waiting for the Indian government's latest draft legislation on crypto assets, which will provide insight into the level of legality offered to these assets. Once it's released, we can fully analyse whether it takes into account the complex and multi-dimensional nature of crypto assets.

Conclusion

Despite the lack of specific crypto asset regulation in India (and the regulators’ shifting attitudes towards web3 - which has had a negative impact on the industry), the sector continues to thrive owing to its internet-native, borderless, open-source and tamper-resistant nature.

Since India is a major player in the global tech industry, it should take a proactive and pragmatic approach towards regulating web3 and its underlying asset classes. Here’s why:

India has a strong interest in promoting its web3 industry to compete with other major economies. Blockchain technology can digitise currencies, stocks, bonds, and other capital assets, creating a “financial internet” which, if properly harnessed, can increase India’s economic and political influence.

India already prefers open-source and “public good” assets over proprietary software (note the huge benefits generated through the India Stack, which is a “public good”), and can position itself as a leader in the new internet, by favouring open-source code, open protocols, and permissionless distributed ledgers as a worthy addition to its domestic application ecosystem.

The MeitY and NITI Aayog papers showcase real-world use cases for blockchain technology, such as finance, logistics, digital identity, legal entities, and property ownership recording. Startups in India are working on building solutions for these use cases. With progressive government support, such projects can have a significant impact in India and globally. As highlighted in Hashed Emergent’s investment thesis, blockchain technology can help turbocharge growth in emerging markets like India.

The web3 industry could add USD 1 trillion to India’s GDP, and is projected to reach USD 10 trillion in the mid-to-long term. As an aspiring welfare state with the world’s largest population, India cannot ignore the potential economic and social benefits of this industry. Over-regulation could result in India losing trillions in economic growth, so it is important to approach regulation wisely.

There has been a brain drain of web3 talent from India due to the government’s stance, and this is a very unfortunate trend that the government must reverse now – with some exceptions, the first generation of Indian tech talent found opportunity and excelled on foreign shores, not in India, and this is surely something that should not be repeated in the web3 space.

A clear and supportive regulatory framework for web3 would not only help attract more innovation, investment, and talent, but would also provide a solid foundation for the development of newer technologies that could have a significant positive impact on India’s society and economy.

These are good reasons why India should not return to a conservative or regressive approach to web3 regulation.

As the Indian web3 industry matures amidst the ongoing bear market, and is visibly rebounding from the previous regulatory mishandling, Indian regulators should adopt an approach based on “technologically informed” principles and aligned with global standards, and spur innovation instead of stifle it.

There are soft signals that the next round of regulation will be more benign, but as always, the devil will be in the details.

Memes speak louder than words, and this one neatly communicates this article’s message:

| A guest post by

|

| A guest post by

|